Lessons From the Great Inflation of 1973-81

Lessons From the Great Inflation of 1973-81 Read More »

A discussion of fractional ownership and Delaware Statutory Trusts for a 1031 exchange

Delaware Statutory Trusts for a 1031 exchange Read More »

Prassas Capital has been involved with renewable energy, and specifically waste-to-energy, finance for the past ten years. We have focused on project finance, rather than financing the companies themselves. We have worked with scores of bootstrap developers, attempting to develop and finance projects throughout the range of waste-to-energy alternatives. We successfully financed two anaerobic digestion facilities, with the participation of a marque private equity firm, in 2015. We repeated secured financing for another biogas developer, for several projects throughout the country. Our engagements have been on a success fee basis, with no monthly retainer required. We appreciate the extraordinary development expenses a bootstrap developer must somehow fund upfront, and we had confidence in our ability to recognize viable (and fundable) projects. There is a renewed interest in waste-to-energy throughout the world, but such projects have unique and stringent financing requirements. Many budding developers, particularly those from a wind, solar or real estate background, underestimate the operating and technological risk, and seek financing on conventional terms. About half the projects we see cannot be financed on any terms. Waste to energy and recycling projects have a high failure rate. This has an enormous influence on the reception by lenders and third-party equity providers. A technology provider is not enough. The project needs an EPC with the financial capacity to offer performance guarantees. The operator must be able to demonstrate ongoing operating capability. A technology is proven when it can operate on a commercial scale. Feasibility studies and white papers have no value in the financing market. Pilot plants offer some validation, but are not proof of concept. They too frequently fail at scale up. Most conventional project finance is real estate or asset-based, which offers a high investment recovery rate if the project should fail. Waste-to-energy projects have little or no marketable assets or real estate. A failed project is virtually a complete write-off. Generally speaking, lenders are not comfortable with waste to energy on a project finance basis. Smaller lenders do not understand them; larger lenders are only interested in larger (greater than $50-$75 million) projects from larger clients with established or desirable relationships. Highly leveraged projects, in the current market, are a myth. We are frequently contacted by budding developers seeking high leveraged loans, and investment tax credits for the entire equity contribution. Â And unfortunately, some investment banks promote such nonsense. Eligibility for tax-exempt bond financing does not alter the loan underwriting criteria. Mutual funds and bond investors are not dumb money. We have seen a number of investment banks issuing term sheets for such projects. Investment banks are financial intermediaries. A term sheet from an intermediary is not only useless, it is deceitful. Only a term sheet from a direct lending or equity source that has the actual capability to write a check, has relevance. Many private equity firms in alternative energy state that they are interested in waste-to-energy; but what they really want is wind and solar, which they (think) they understand and is considered risk-free. Few financial investors understand the technology and operating risks behind WTE, and are ultimately unwilling to close. Developers must generally have their own early stage pre-development money. Viable projects require long-term feedstock and offtake agreements. Merchant facilities are exponentially more difficult to finance. Unlevered project IRR of high teens to mid-twenties is necessary to attract private equity. While investment tax credits are generally available for larger wind and solar projects, waste-to-energy is often considered too risky. Investment tax credit providers want equity returns with debt security. Their terms and conditions often conflict with and are incompatible with debt.

Why waste-to-energy projects fail Read More »

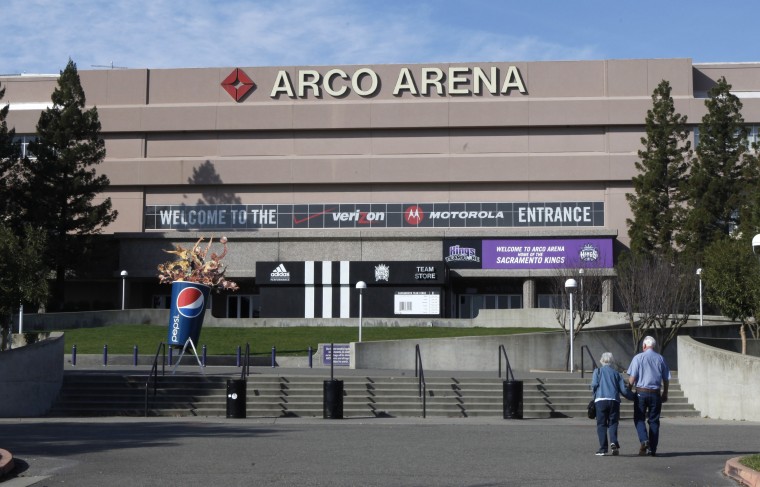

In 1988, I was working in San Francisco, desperate to escape the drudgery of proposals and spreadsheets that define an apprenticeship in investment banking. Like a struggling actor waiting tables, I was looking for that one break, that one deal, to launch my career. That deal was the Arco Arena. Once upon a time, sports stadiums and arenas were municipal projects, underwritten by the taxing authority of the resident city or county. No commercial lender would approve a project entirely dependent on event-driven revenue like ticket sales and popcorn purchases. These projects required the deep pockets of the local community. The economics of all that changed with the advent of luxury skyboxes. Team owners discovered that creditworthy corporations were willing to sign rather expensive long-term leases to watch an event in a private, luxurious setting, with real food and their own bathroom. Build enough of these skyboxes, and the aggregate lease revenue alone was enough to pay the debt service on a larger, modern facility. The team owners could build and own the facility, and keep that new source of revenue, rather than plead with the local community for a new venue. More importantly (from a banker?s perspective), the financing was no longer dependent on unreliable, event-driven revenue, but rather the stable income from credit-worthy lessees. The financing was packaged and marketed to emphasize the skybox revenue as the foundation of the debt security. The Fuji Bank, then a AAA-rated commercial bank, came aboard to credit-enhance a five-year taxable bond, which priced at 10% (a terrific interest rate at the time). Perhaps a new concept is the notion of packaging and marketing a financing by differentiating, and segregating, assets and income streams. In its most basic form, it is fundamentally no different than a real estate owner who seeks financing by emphasizing his anchor tenant. If a financing is straightforward, easily understood, and if you have a smart banker, the packaging may not matter. However, every lender?s reaction to a financing with an unfamiliar structure, collateral or revenue stream; which might (for any reason) elicit the perception of heightened risk, is to require an additional cushion of safety: more collateral, more control, and a higher interest rate, if indeed they remain interested at all. Even for the most creditworthy projects, it is customary for a lender (unconstrained by competition or negotiation by an experienced client) to place a blanket lien on all revenue and every asset, and even require additional recourse to third-party guarantors. This obviously protects the lender?s interest, but at the direct expense of the borrower; as it limits the organization?s ability to secure future financings, at least not without replacing the original lender at potentially considerable expense. A skillfully packaged financing has one agenda: clearly illustrating mitigated risk to potential lenders, in such a way as require the encumberance of the fewest possible assets and revenue streams. Skyboxes changed the math, and changed the game, launching a sports stadium and arena construction boom that lasted for decades. The Arco Arena financing gained some notoriety and received mention in The Wall Street Journal. Concurrently, the Palace of Auburn Hills (home of the Detroit Pistons) financing, achieved through the same skybox revenue emphasis, was completed in that same year. The concept took off. I subsequently spent several years traveling and meeting team owners throughout the country. I am not a spectator sports fan. In fact, I find professional sports to be unbearably boring. When the owners invited me to watch an event from the owners box, I would decline, on the premise that I had to maintain my objectivity. And I was complimented on my professionalism. Alas, the purely private concept did not endure. Team owners quickly realized that it never pays to let a patsy off the hook, and almost immediately used the skybox revenue and the new form of financing as leverage against the vanity of local politicians to demand greater public funding, in the form of public/private partnerships, to construct ever grander facilities. Al Davis was the emperor of the technique, bluffing four California cities into offering the Raiders extraordinary compensation packages without taking a penny of risk himself. Soon, it became very difficult to get momentum on any project, as every team owners? vanity was suddenly at stake to become the next master of the universe. Every Wall Street firm poured into the new sports facility financing business, and every completed deal spawned a dozen new consultants who were now facilities experts. The early deals, absurdly lopsided on behalf of the sports teams, could arguably be excused as a learning exercise for municipalities who were bolstered by an academic rationalization that such public projects were an essential catalyst for economic redevelopment. The City of Oakland and Alameda County, for example, ultimately spent hundreds of millions of dollars to attract and retain the Raiders, tax dollars that otherwise could not be spent for other local public services. Of course, in most cases, the redevelopment catalyst was illusory. There were no consequences to the careers of the political sponsors and advocates who squandered public funds. It was apparently not even a learning experience. Currently, Sacramento struggles with a new ownership group threatening to move the Kings (article here), while the Minnesota Vikings are demanding a new one billion dollar facility.

Packaging Risk: How I Financed the Arco Arena Read More »

A Tale of Two Clients In 2006, I met with two potential corporate clients. Coincidentally, they had about the same annual revenue, were in the same industry, and were located in the same broad metropolitan area. Each wanted to borrow about $10 million for capital (long-term) projects. I?m not sure why the first prospect even requested the meeting. A dominating board member had already decided to borrow from a local commercial bank, for a five-year term. The bank, in addition to the usual collateral demands, also wanted personal recourse from several of the principals. A discussion of financing alternatives was met with an argument, or outright doubt that other viable alternatives even existed. The chief financial officer of the second client considered the alternatives, and the associated trade-offs, and chose a thirty-year, fixed rate, non-recourse bond issue, privately placed with one mutual fund. Then the credit crisis struck in 2008. The businesses of both clients suffered in the aftermath. Interest rates spiked as all financing alternatives evaporated. The first client?s business failed to sufficiently improve by the time the bank loan matured in year five. The bank would not renew the loan, at a time when even credit-worthy borrowers found it difficult to secure financing. The client tried to negotiate, but the bank had no incentive to do so, since it had recourse to the principals. The bank ultimately foreclosed, and seized the collateral from both the company and the guarantors. The second client was initially indifferent, since long-term fixed rate financing by definition sidesteps any refinancing risk. Then they realized that bonds, unlike bank loans, are marketable securities, and that bond prices fluctuate with changes in market interest rates. More specifically, the price of the bond issue they ?sold? a few years ago had fallen precipitously as interest rates spiked. The client subsequently negotiated with the mutual fund and bought back their bond at a tremendous discount. The mutual fund was a willing participant, since they trade their portfolio and are accustomed to profits and losses in any given market. The client dramatically lowered their outstanding indebtedness, improving their cash-flow and competitive position for the coming years. Granted, this example lacks the high drama of a merger or hostile takeover. But reality tends to be boring, and these types of capital raising assignments are the bread and butter of investment banking. And unfortunately, the two clients in this example are not unique. My business practice often involves an endless round of educational meetings with clients and prospects who may not appreciate the nuances and ?bets? inherent in their financing alternatives; or the fact that markets (and opportunities) change, and at times may even contradict their own past experiences. For example, it?s easy to dismiss the board member of the first client as a jerk who wouldn?t listen. In fact, he was a wealthy entrepreneur who had worked with this particular bank for many years to build his own business. The short-term bank loan carried a slightly lower interest rate than long-term bonds, which he valued for the immediate cash-flow savings. For the last thirty years, lenders have always lent and interest rates have always fallen. He knew what worked. And if it?s not broke… The capital markets, of course, have always been far bigger than just the local commercial bank. But these days, the game has changed. Maybe not changed, but certainly shifted. This series of posts will discuss capital raising in the post crash environment, from inside the sausage factory. I?ll spend more time on borrowing, because borrowing is far more prevalent than raising equity, and far more institutionalized. If you follow certain rules and meet certain criteria, you can always find money to borrow. Raising equity is different. We?ll discuss that in a separate series. I will not spend much time on exotic or specialized forms of debt, other than perhaps to note their existence. Rather, this discussion will simply reflect the discussions I routinely have with current and prospective clients. I tend to think of lenders as single-cell organisms (and I?ll bet most lenders would agree). They are simple creatures, and if you internalize some very basic concepts, it will make the process much less aggravating. [list type=”list1″] Lenders are not venture capitalists. They will not ?invest? in your business. They have no incentive to take business risk. Think about it: under the best of circumstances, all they get is their money back, with some interest. Your borrowing – your eligibility, the rate, the terms – all depends on the lender?s perception of downside risk . Lenders are not perfect. They mis-perceive risk. And 1% of the time, they do go insane. The recent real estate bubble is an example. Unfortunately, everyone in need of financing spends too much time looking for that one insane lender. It is a wasteful and often futile approach. Shop around, but keep in mind that lenders are sheep, and tend to look at the world with the same risk-averse mindset. If you are creditworthy, you have options. If you are not creditworthy, you may not have any options. It is surprising how often a client, with no net revenue and no collateral, will insist on a non-recourse loan at interest rates comparable with Treasuries. The availability of construction financing will directly depend on the evidence of take-out financing. ?If there is bankable take-out financing in place, it is very easy to find construction lenders. ?No evidence of take-out financing, no construction loan. There is no free lunch. There are trade-offs. Listen for the trade-offs. Variable rate loan rates fluctuate in both directions. ?A twenty year loan with a five year put is really a five year loan. Strong commercial banks have the capability to offer non-recourse loans to creditworthy projects. ?Weak banks will always insist on recourse. Lenders are not objective financial advisors. They are not looking out for you. They are looking out for themselves. Loan officers (investment bankers, whatever their title) have an employer. They have a

Press Release. October, 2009 Kapolei, Hawaii: Six months ago, Island Pacific Academy was like many start-up independent schools. Even though it had enrolled 650 students PK-11 in four years of existence, it struggled to meet the debt service on a $20 million bond issue amidst rising costs and the stagnant enrollment of the current recession. Today, the School has cash reserves and completed the purchase of its property. The debt remains, but the debt service is more manageable, given the school’s comparatively low tuition and enrollment. How did they do it? “Bond math 101”, says Nick Prassas, financial advisor to the School. Two years ago, the School sold a bond issue at par, at a low fixed interest rate. When the credit crisis hit, interest rates spiked higher. Higher interest rates, lower bond prices. The School was able to negotiate the repurchase of its bond issue from bond holders at a substantial discount. Of course, the School still needed a source of funds to buy back their discounted bonds. That source: federal stimulus dollars from the United States Department of Agriculture. “We were at the right place at the right time,” says Stuart Hirstein, Associate Headmaster and Chief Operating Officer. The USDA, which provides rural community facilities financing, became one of the conduits for disbursing federal stimulus funds. The agency, having guaranteed a loan for the School several years ago, was already familiar with our financial profile. We made our request just as stimulus funds were being allocated. The USDA funds came in the form of a direct loan, and a loan guarantee. The direct loan carries an interest rate of 4.5%, repayable over forty years, instead of the customary thirty. “It sounds straightforward, now that we’ve closed the transaction,” says Dan White, Headmaster of the School. “The USDA program is designed to support new community initiatives. Fortunately, IPA had received a five-year grant from the Hawaii Community Foundation in their Schools of the Future program. The Schools of the Future process will, in fact, transform our school and represent a genuinely new initiative. Putting the deal together, though, required long hours and hard work by several knowledgeable people. The notion of a school capitalizing on the USDA stimulus program to buy back their own bonds at a discount, just one year after selling them, is novel. ?Obviously the recession provided fertile ground for thinking outside the norms of independent school finance, added Prassas. Everything we hear, though, about independent schools in the post-recession world would suggest that the old norms are not likely to return. The schools of the future – 15 to 20 years down the road – might well look very different than today. Why wouldn’t school financing evolve in a similar fashion? asked White. We still need to make enrollment targets, continued White. The debt service is still a huge chunk each month. We continue to be frugal; we have to be. But we have a huge asset our land that we did not have before, and there is great security for the school in that fact.

Lemons to Lemonade: How Island Pacific Academy beat the Credit Crisis Read More »