Commercial real estate has been a fantastic investment for the past ten years or so, and especially now with rising interest rates, investors are beginning to voice the same concerns:

“I’d love to sell my property, if only I knew what to do with the money.”

- Should I continue to hold, or is now finally the time to sell?

- If I decide to sell and just cash out, what kind of tax bill should I expect?

- If I sell and wish to defer all those taxes, will that then force me to buy back into the same overheated market I just sold out of?

- How can I protect my principal? Are there alternatives that may do better during a recession?

The Bigger Picture

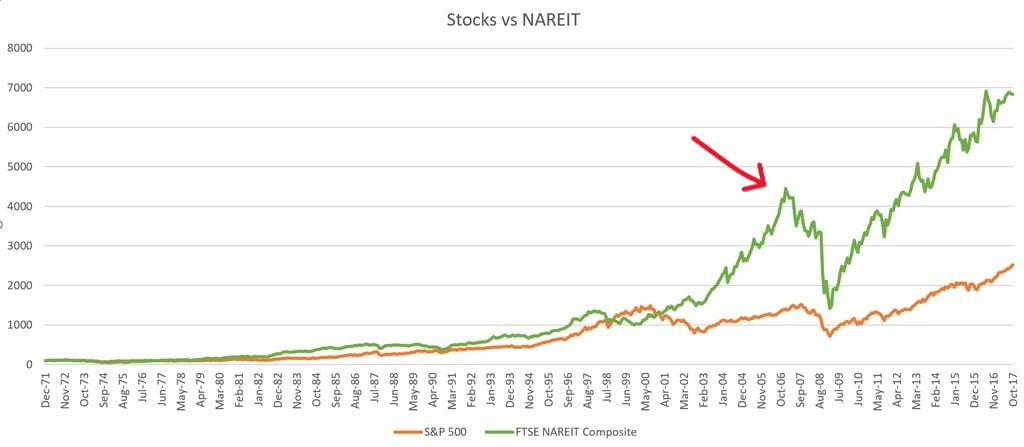

The graph below illustrates the price history of commercial real estate, compared to the S&P 500 (which has not exactly been standing still) for the past fifty years. In particular, make note of 2006 (the red arrow). In this year, real estate was considered to be one of the biggest speculative bubbles in the history of speculative bubbles.

Let that sink in for a moment. One of the biggest bubbles of all time. Bigger than the dot.com bubble in 2001.

Bigger than the stock market bubble in 1929.

And as you can see, we have blown right through those price levels. Note that the graph ends in 2017. Real estate prices have only become more extreme in the past five years.

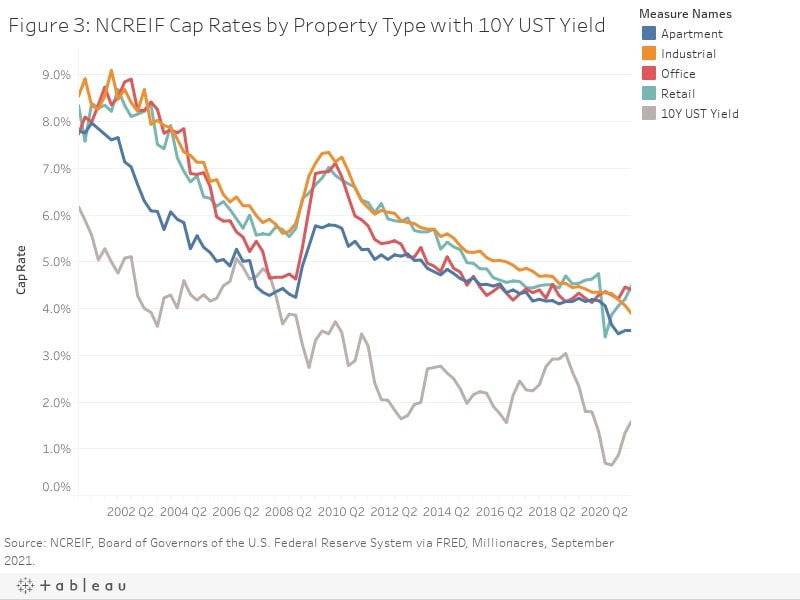

The next graph shows the collapse in cap rates. Cap rates have not only fallen to historic lows, but they have compressed. Junk properties hardly pay much more than investment grade properties.

Borrowing rates are rising, while many real estate sectors are still priced at 3-4% cap rates. Prices must eventually break. It is natural for many investors to at least consider taking some of their chips off the table.

Cashing out – the math: Many investors would like to reduce or eliminate their exposure to real estate, for many reasons – to just cash out. After all, they sacrificed over the years, to be able to invest wisely and grow their wealth over a lifetime. And now that they have reached a stage in life where they can enjoy the fruits of their labor, they discover a rather cruel irony – they are going to get crushed in taxes.

- Federal tax: Capital gains on real estate is taxed at 15-20%. However, many sellers in high appreciation locations may instead qualify for the Alternative Minimum Tax (AMT) at 29%, if their capital gains are disproportionately high when compared to their ordinary income in the year of the sale.

- State tax: State taxes are generally at the ordinary income rate, since most states do not have a separate capital gains rate. State taxes can range from 0-13.3% (California)

- Recapture of depreciation: Depreciation recapture is the portion of the gain attributable to the depreciation deductions previously allowed during the period the taxpayer owned the property. The depreciation recapture rate on this portion of the gain is 25%.

- Total: The aggregate taxes due on a highly depreciated property can exceed 40% of the net sales proceeds.

- The investor still has a reinvestment decision with the after-tax proceeds.

Installment sale: Some investors mistakenly believe that an installment sale will address their tax and reinvestment problem. It does not. I have written a separate article specifically on installment sales.

1031 Exchange, and defer the taxes: Most investors are understandably horrified when they discover the magnitude of their total tax bill. However, there is another option.

Commercial real estate has a special feature in the tax code, unique from any other asset class. An investor can sell their property and defer all the taxes (including depreciation recapture) if they reinvest the proceeds in a like-kind property, within certain time limits. (like-kind is defined as another real estate asset of a similar nature). An investor can hypothetically continue to buy and sell property, exchanging into the next purchase and deferring all tax liability, over a lifetime. At the end, when their heirs inherit the property, the cost basis is stepped up and the deferred tax liability is gone for good.

Given the tax consequences of cashing out, a 1031 exchange is a compelling alternative. However, it is not without its unintended consequences.

- The IRS exchange rules force an investor to buy back into the same real estate market they just sold out of, within a very short window of time. This may be inconsequential, if the purchase is for a business purpose, or if the investor is diversifying their re-investment in various other markets or property types. It is very consequential if the investor is investing right back into the same over-priced market they just sold out of.

- Many, if not most, investors have done quite well over the past few years. Often, they can be over-confident in their continued good fortune, and so eager to avoid paying taxes that they rush into an exchange without perhaps the care and due diligence they exercised when contemplating the initial purchase. In their haste to avoid paying 40 cents in taxes, they jeopardize their entire investment dollar in an ill-conceived exchange.

In 2006-2008, at the height of the last bubble, and currently within the past two years, I have noticed a troubling tendency among prospective clients, flush with capital gains and contemplating their next purchase.

- Some investors have done so well, so quickly, that they no longer have a genuine fear of risk. They believe real estate may experience a few bumps, that it may appreciate more slowly than in the past, but it will appreciate. The prospect of an actual loss of principal is unthinkable. On the contrary, they anticipate doubling their money yet again.

In the aftermath of the dot.com bubble, many of my friends and acquaintances, upon calculating their investment losses, lamented, “What was I thinking? Never again.” I heard the same refrain in 2009, after the real estate bubble. “It was so obvious. Never again.” Clients now tell me that 2009 can never happen again. “This time it’s different.”

Think about that.

- A second, more prevalent and more insidious tendency, is reaching for yield. Reaching for yield is a classic investment pitfall, one that is taught in finance courses. It is a pitfall that professionals are just a likely to commit. Pension funds are often just as guilty as individual investors, and pension funds know better.

Many investors live off the net income produced by their real estate portfolio. And it is only natural to want more income. Unfortunately, we now live in a low yield world. Falling yields have been a bonanza until recently, because it has resulted in vastly higher asset prices. But now investors want to sell their low cap rate property, and re-invest in a high cap property. What is often ignored in the equation is that high yield means high risk. And during a period of compressed cap rates, higher yields often result in much higher risk.

Too many of my clients look at yield first and foremost. They do not equate yield with relative safety or risk, they focus on the amount of income they need, or hope to get. They reach for yield, without particular regard for the underlying dynamics of the market or that particular property.

In a recession, the riskiest assets are those most vulnerable to fail – high yield bonds, start-up companies, and high yield real estate. Is it impossible to find low hanging fruit, or a viable turnaround situation? No. Is it likely? If anything is trading at a significantly higher yield than the market, it is important to know exactly why. Especially after a bull market, it is very easy to underestimate risk. And most people do not nearly have the risk appetite they think they have.